On September 27, 2024, Governor Newsom signed Senate Bill (SB) 219 into law, reaffirming the reporting timelines for 2026 under both the Climate Corporate Data Accountability Act (previously SB 253) and the Climate-Related Financial Risk Act (previously SB 261), now collectively known as the Climate Accountability Package. This move reaffirms strong support for US mandatory climate disclosures, even as momentum around such regulations has slowed.

The ongoing Chamber of Commerce of the United States of America v. California Air Resources Board lawsuit, which seeks to block these requirements, adds legal uncertainty. However, companies are urged to continue preparing, as the regulatory framework progresses despite this challenge.

As Q4 2024 progresses and the window for preparation shrinks, companies must act now to ensure readiness.

While there are some minor updates from SB 253 and SB 261 to SB 219, the core requirements of the bills remain largely unchanged.

SB 219, Climate Accountability Package |

SB 253, Climate Corporate Data Accountability Act |

SB 261, Climate-Related Financial Risk Act |

|

| Who? | No change from SB 253 and SB 261 | Businesses with revenue exceeding $1 billion and operating in California | Businesses with revenues exceeding $500 million and operating in California |

| Deadlines |

Changes made only from SB 253 (Scope 3 emissions):

|

Scope 1 and 2 emissions:

|

Publish first climate-related financial risk report on or before January 1st, 2026 |

| Frequency | No change from SB 253 and SB 261 | Annually | Biennially |

| Reporting changes |

Change made only from SB 253: Permits entities the option to consolidate GHG emissions disclosures at the parent- company level |

Option to consolidate reporting at the parent company-level was not specified. | Permits entities to consolidate reporting at the parent company-level |

Other minor changes in the bill focus on providing greater flexibility to the California Air Resources Board (CARB).

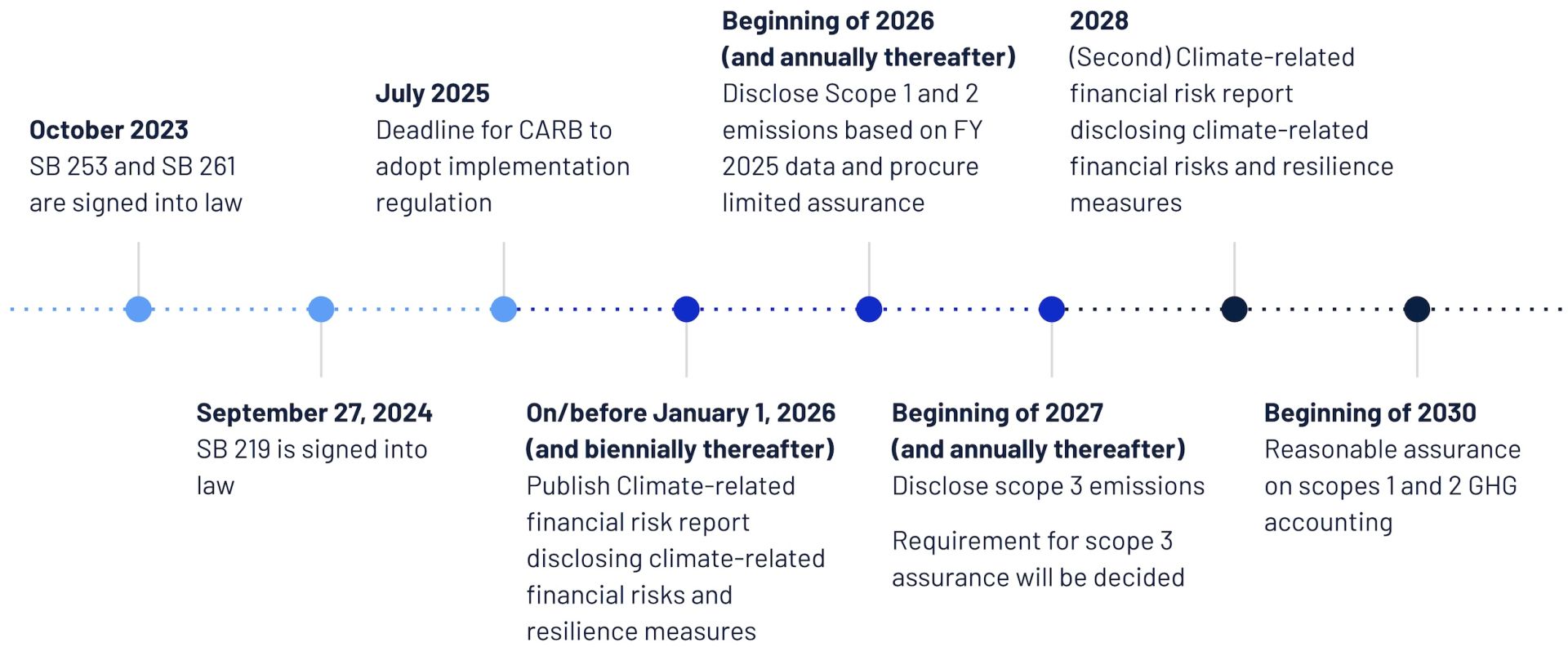

SB 219 compliance timeline

To comply with California's climate disclosure regulations, companies must first assess if they qualify as ‘doing business in California’ to determine if reporting is required. Those within scope should spend the rest of the year identifying compliance gaps and preparing a 2025 plan to meet 2026 reporting requirements for Scope 1 and 2 emissions, as well as climate-related financial risks. This plan should include calculating emissions and possibly conducting a Scope 3 screening for the 2027 disclosure.

To address climate-related financial risks, companies should start with a climate risk screening and follow up with a climate scenario analysis to assess potential climate-related financial impacts. Based on this, they can then develop strategies to mitigate and adapt to the identified climate risks.

Companies operating across jurisdictions should align with all relevant climate disclosure regulations simultaneously to streamline reporting and close compliance gaps. This approach is particularly efficient given the overlap between SB 219, the Corporate Sustainability Reporting Directive (CSRD), and IFRS S2 standards. South Pole’s climate reporting experts can help your business navigate global regulations and create a tailored regulatory readiness roadmap.