Over the last few years, we've seen a wave of new initiatives and regulations emerge surrounding climate-related financial disclosures across the globe. These assessments provide companies with a clearer understanding of the strategies they need to implement, while also providing investors with more information and data to make informed decisions around their climate risks. For example, wildfires, floods, or changes in policy and regulation could negatively affect a borrower's ability to meet debt obligations or make assets inaccessible or uninsurable, affecting a business's ability to operate and value.

This influx of new regulations reflects the growing importance of standardised, transparent climate-related disclosures in the global financial system.

But how did all of these disclosure rules come about? What do all the regional rules require? How does this impact your organisation?

There are two main governing bodies for climate-related financial disclosures: the TCFD and the ISSB.

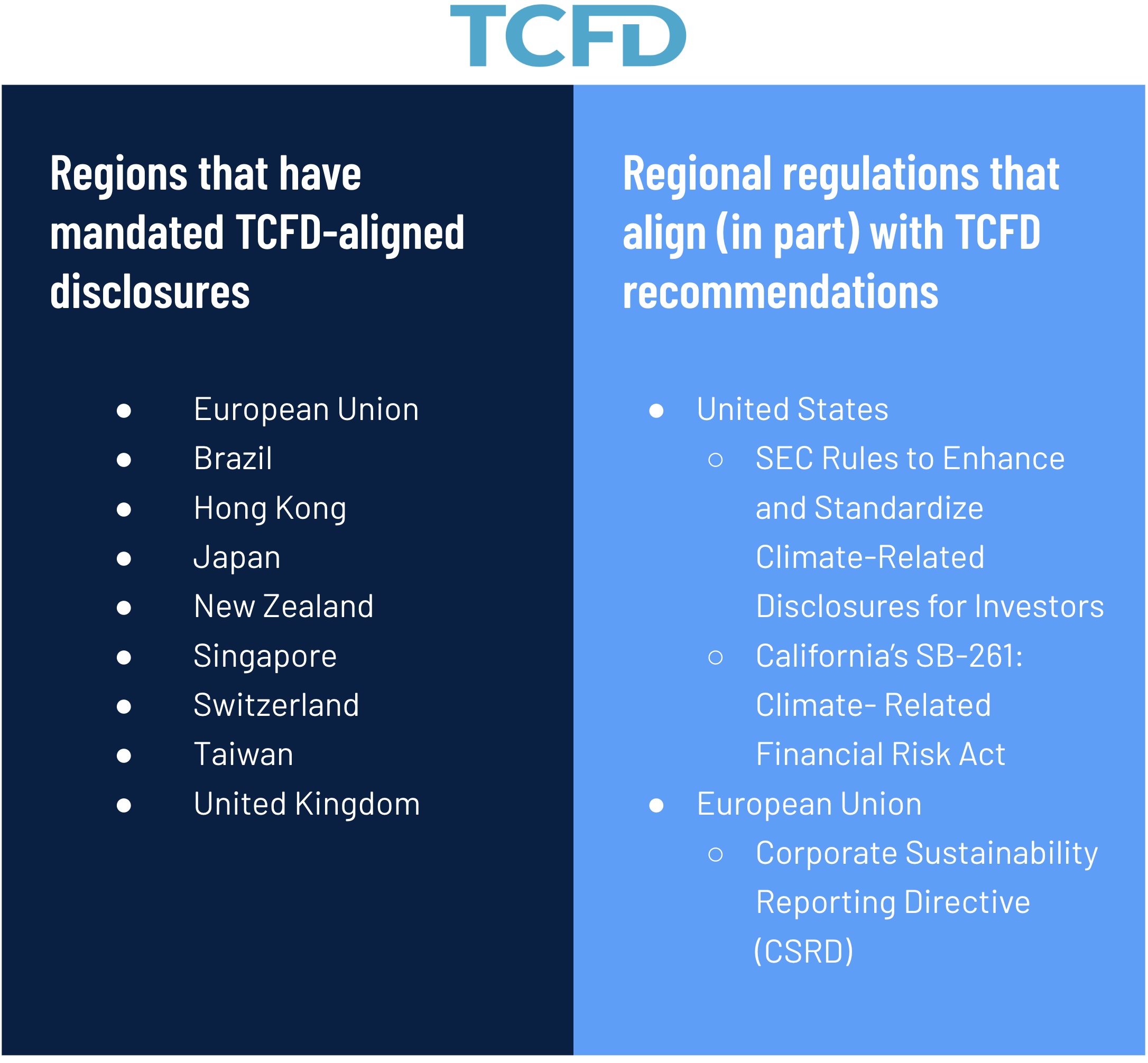

In 2015, the Financial Stability Board (FSB), an international body that monitors and makes recommendations on the global financial system, launched the Task Force on Climate-related Financial Disclosures (TCFD). The TCFD's primary mission was to create a framework that would enable organisations to increase transparency and more effectively disclose climate-related risks and financial data. The TCFD's recommendations, released in 2017, have since become a cornerstone for many climate-related reporting initiatives and regional regulations. Numerous countries now require mandatory coverage of TCFD recommendations, and others have based their climate-related disclosure laws in part on TCFD recommendations.

In October of 2023, the FSB announced the TCFD had fulfilled its mandates and disbanded, transferring the role of monitoring the progress of companies' climate-related disclosures to the International Financial Reporting Standards (IFRS) Foundation, a non-profit that oversees financial reporting standard-setting.

The IFRS established the International Sustainability Standards Board (ISSB) in 2021. The ISSB was given the task of creating a harmonised, global baseline for sustainable reporting due to growing demands by investors, companies, and international policymakers. In June 2023, the ISSB issued its first two standards: IFRS S1 General Requirements for Disclosure of Sustainability-related Financial Information and IFRS S2 Climate-Related Disclosures.

These new standards reduce the complexity that the TCFD recommendations presented, giving companies more consistent and reliable climate risk data to help them make decisions.

Many countries are now in the planning or consultation phases of requiring mandatory coverage aligned to ISSB recommendations. Some select countries, namely Australia and Malaysia, have regional recommendations based in part on ISSB recommendations that are being reviewed and will be presented soon.

With the growing number of frameworks and regulations, it is easy to feel overwhelmed by the "alphabet soup" of climate-related disclosures. The good news is that these frameworks share key similarities and provide best practices, making it easier to navigate the reporting landscape.

Use our map to see if your organisation has been or will be impacted by the regional disclosure frameworks.

Companies should adopt an iterative approach to climate-related risk disclosure. This involves continually refining practices by regularly evaluating and updating the disclosed information. This ongoing process, informed by the latest developments, emerging risks, and stakeholder feedback, ensures the sustained relevance and technical accuracy of the disclosed data.

Furthermore, companies can mitigate climate risks and seize opportunities with a well-crafted climate transition plan. This strategic roadmap serves as a blueprint for transformation – it outlines an organisation's journey towards its climate targets and goals, as well as how they will adapt to climate change impacts and emerging opportunities.

The good news is that significant progress has been made in creating standardised approaches to climate disclosures. Understanding these governing frameworks from the start will allow your company to comply with the regional disclosure mandates while providing the right information and data to make informed, climate-resilient decisions. Armed with this information, companies and investors that move early will be able to turn climate risks into business opportunities and leapfrog competitors.

To support your organisation in implementing best practices for climate-related reporting, South Pole offers the following services:

Climate risks and opportunities have the potential to impact businesses' financials, which may be required to disclose. Are you already assessing them?

Australian Sustainability Reporting Standards

Mandatory for largest listed and unlisted companies and financial institutions for 2024-25 financial

year, with phased reporting for other entities to FY2027-28.

Download South Pole's Quickguide to the ASRS here

Starting 1 Jan 2024, banks and financial institutions must begin implementing ISSB standards.

Publicly traded companies.

The proposed standards allow public companies and investment funds to begin sustainability reporting following the IFRS Standards in 2024 on a voluntary basis, with mandatory reporting for public companies to begin in 2026.

From 2027, sustainability reporting will be required within three months after the end of the fiscal year or simultaneously with the release of financial statements, whichever occurs first.

The proposed standards would become voluntarily effective for Canadian companies' annual reporting periods beginning on or after January 1, 2025.

Regulated entities will be required to apply the ISSB standards from January 2025, and entities that are classified as high tax payers will be required to apply the standards from January 2026.

Regulated entities: companies with a public obligation to render accounts, supervised and regulated by CONASSIF (National Financial System Supervisory Board).

ESG disclosure rules that broadly align with TCFD pillars, IFRS baselining, and supports interoperability guidance from IFRS and European Financial Reporting Advisory Group (EFRAG).

Requires companies with business in the EU to collect and report their sustainability data with a phased in approach:

Download South Pole's Quickguide to CSRD here

All listed companies in Hong Kong

New Climate Requirements (added to Hong Kong's ESG Code)

The HKEX requires all listed issuers to report Scope 1 and 2 GHG emissions starting from FY2025 .

For Scope 3 GHG emissions and other disclosures other than Scope 1 and 2, there is a one-year interim transition time for large cap issuers, from a comply or explain basis in 2025 to mandatory disclosure in FY2026. Main board issuers other than large caps follow a comply or explain basis commencing on or after FY 2025, whereas disclosure is voluntary for Growth Enterprize Market (GEM) issuers.

All listed companies in Japan

The proposed standards would be mandatory for companies listed on the prime market of the Tokyo Stock Exchange, under Japanese securities laws and regulations.

New Climate Requirements (added to Hong Kong's ESG Code)

There's a phased in approach for Main market listed issuers and ACE Market listed issuers.

ACE Market - Bursa Malaysia's sponsor-driven market, designed for companies with growth prospects, was repositioned from the MESDAQ Market after August 3, 2009. Sponsors evaluate potential issuers based on their business prospects, corporate conduct, and internal control adequacy.

Main market - Prime Market of Bursa Malaysia is for established companies that meet specific standards of quality, size, and operations. Potential issuers must demonstrate either a minimum profit track record or a market capitalization of at least RM500 million upon listing.

Requirements will be introduced in a phased approach:

Large non-listed entities whose parent company already reports climate-related disclosures using ISSB-aligned local reporting standards or equivalent standards (e.g. European Sustainability Reporting Standards) will be exempted from reporting and filing climate-related disclosures, subject to certain conditions.

Consulted disclosure rules would be required for all listed companies in Singapore.

All domestic listed companies, financial institutions, and some others (e.g. SMEs) are required to use Sri Lanka Financial Reporting Standards, which are IFRS Standards with some modifications.

Public companies, banks and insurance companies with 500 or more employees and at least CHF 20 million in total assets, or more than CHF 40 million in turnover.

Companies listed on the TWSE (Taiwan Stock Exchange) and TPEx (Taipei Exchange) .

Among the businesses included in the "List of Enterprises Listed in the First Paragraph of Article 3 of the Board Decision and Subject to Limits";

Businesses that exceed the threshold values of at least two of the criteria in two consecutive reporting periods are included in the scope of mandatory application.

2) In accordance with the Banking Law No. 5411 dated 19/10/2005, banks subject to the regulation and supervision of the Banking Regulation and Supervision Agency are within the scope of mandatory reporting without being subject to any threshold value, even though they are listed in the list below. However, banks within the Savings Deposit Insurance Fund are exempt from this practice.

Climate-related Financial Disclosure

Mandatory for UK Public Interest Entities (PIEs) and Alternative Investment Market (AIM) listed companies with over 500 employees, as well as UK private companies and LLPs with over £500m in turnover and 500 employees (including subsidiaries)

Portions of the rule are modeled after TCFD.

This rule applies to all companies registered with the SEC. This includes:

Read more about the SEC final climate disclosure rules in our blog

California's SB-261: Climate-Related Financial Risk Act

Rule aligns directly with TCFD recommendations.

Any corporation, partnership, limited liability company, or other business entity formed under the laws of the state, the laws of any other state of the United States or the District of Columbia, or under an act of the Congress of the United States with total annual revenues in excess of $1 Billion USD and that does business in California.

Read more about complying with California's climate disclosure laws here

Large publicly listed companies, large insurers, banks, and investment managers