The trend for global corporate PPAs transactions has been positive for over a decade. Growing awareness of the tremendous benefits of PPAs – from achieving corporate reduction targets to hedging against price volatility – has attracted more corporate buyers, resulting in consistent year-on-year growth of transactions.

Businesses have been able to use PPAs as the centrepiece of their scope 2 reduction strategy, whilst also benefiting from the long-term electricity price certainty they provide.

During the past two to three years, however, energy markets have experienced unprecedented volatility. The disruptive effects of the global COVID pandemic at the start of 2020, which led to significant demand destruction and historic low energy prices, was followed in 2022 by historic high energy prices as a result of Russia's invasion of the Ukraine and the resultant loss of Russian gas to Western Europe. Never before in Europe have energy buyers been exposed to such significant price swings in such a short period of time.

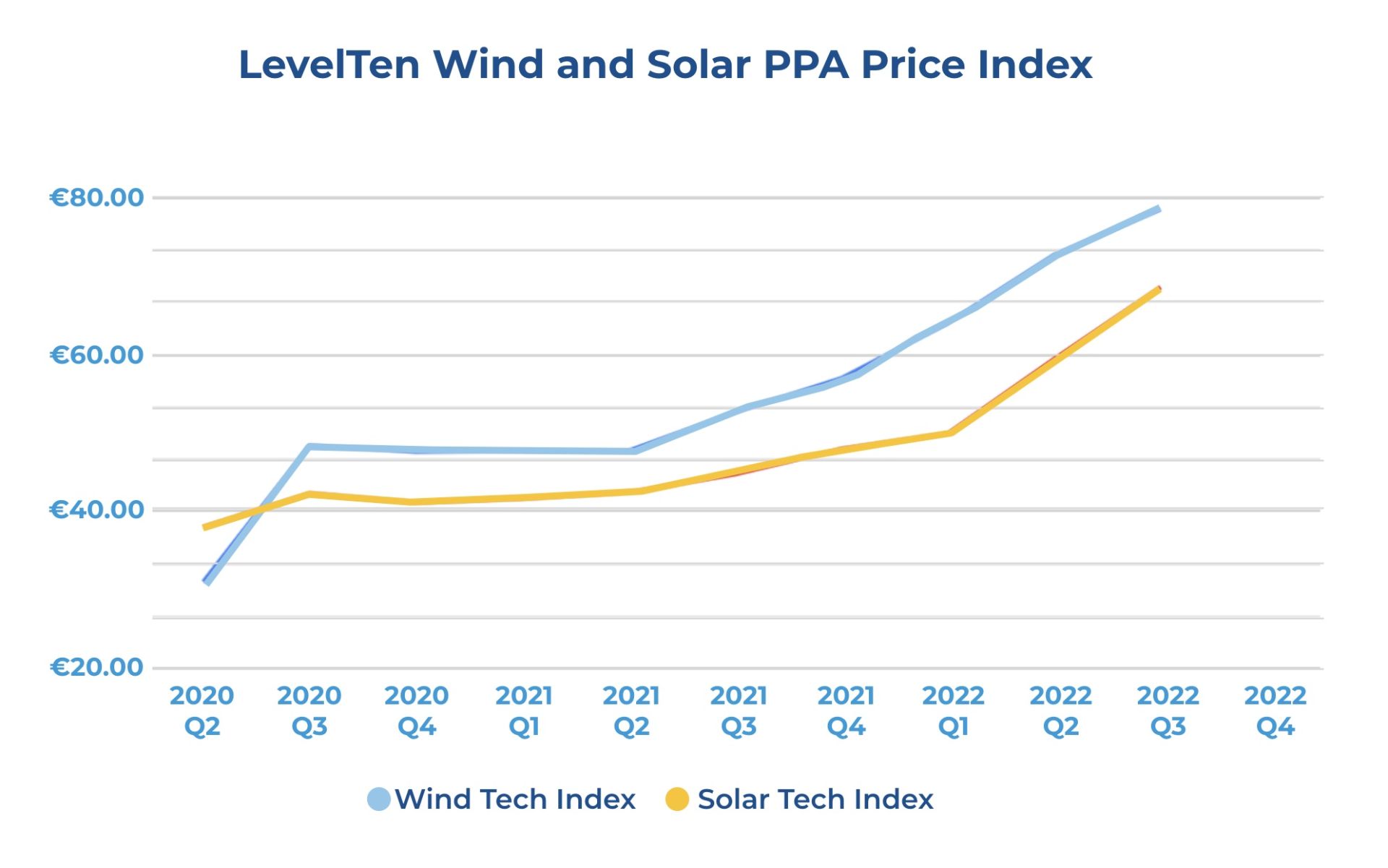

A rise across commodity markets has meant rising costs for renewable energy project developers, who have been forced to pass on these cost increases to buyers, causing considerable disruption to PPA markets. Consequently, PPA prices have increased significantly across all regions in the past 12 months. According to LevelTen's price index of average PPA prices, prices increased by 23% for wind and 37% for solar in Europe in the period from Q1 to Q3 2022. In North America across the same period, prices increased by 14% for wind and 16% for solar.

Growing corporate interest in PPAs, coupled with the recent energy price shocks, have pushed the market to flip from a buyers market to a sellers market. PPA buyers are being forced to re-evaluate their sourcing approach to make sure that the time and effort they invest has the best chance of success. In today's PPA markets, more than ever before, full preparation prior to formal market engagement is critical – this is the key to making the process as expedient and efficient as possible.

Although PPAs still offer the potential to beat the market, based on comparisons with long-term energy price forecasts, buyers should bear in mind the following challenges and imperatives:

Getting everything ready before you release a formal tender is key. First, ensure your internal stakeholders are educated about the various PPA types and pricing structures available, as well as the risks and opportunities associated with them. Any potential hurdles presented by credit provisions and accounting should be weighed up beforehand, and ways to mitigate and manage these challenges should be explored and agreed upon. Furthermore, gathering initial data around project availability, market pricing and the associated business cases across all relevant geographies will help set realistic expectations about what can be achieved during a sourcing process.

Good PPA strategies are led by data: gathering this and completing the commercial analysis before you put out a formal tender is crucial; this enables you, the buyer, to present real business cases and secure provisional approval based on known commercial thresholds or ranges.

Ultimately, being quicker and being able to act more decisively will greatly increase the probability of securing a corporate PPA in these challenging times.

Our offering focuses on empowering energy buyers with the information they need to prioritise opportunities and present the information to senior stakeholders effectively.