Not only do they finance the protection and restoration of natural ecosystems, projects generating certified carbon credits also play a crucial role in supporting communities disproportionately affected by climate change and in establishing systems and infrastructure for improved future resilience.

Carbon credits are a central element in the corporate climate action puzzle: companies should prioritise setting a 1.5°C science-based target and making absolute emission reductions, but credits allow businesses to take action now to compensate for their residual emissions and, importantly, finance the global transition to net zero.

As outlined in South Pole's principles around credible carbon credit use, and to make sure that climate action is meaningful, it is crucial that businesses purchase high-quality carbon credits. Yet many companies still have questions about how to improve their buying processes: a recent South Pole review of credit purchase RFPs found that ~80% of requests called for some sort of due diligence support.

It seems clear the corporate world is now asking: how do I navigate risk and maximize impact when purchasing climate credits?

Like most investments, the purchase of carbon credits is never 100% risk-free. Common carbon credit risks include those associated with additionality, permanence, and leakage* – and these risks vary based on carbon project types, technologies, and their location.

In addition, in periods of rapidly changing market conditions, the desired credits may not be available when the time to buy comes, and fluctuating prices may limit companies' ability to capitalise on strategic purchases.

Some of these risks are controllable. For instance, a company can choose which types of credits to purchase and therefore can better manage how these risks materialise in practice. While there will always be risks beyond an entity's control (credits of all types can get caught up in a broader press narrative around credit criticism), a tightly run purchasing process based on best practices can minimise these risks.

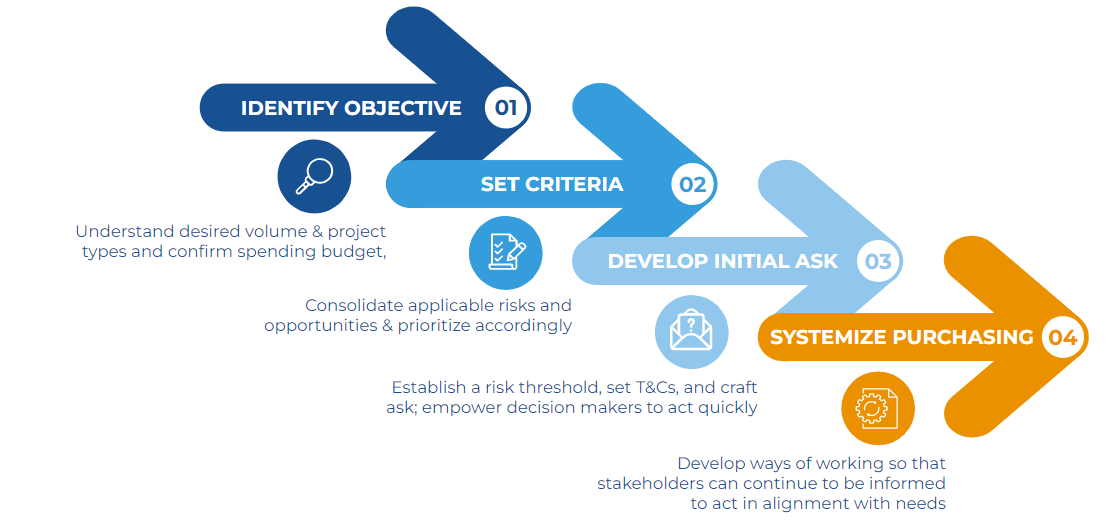

While specific needs may vary across different entities, we recommend that all buyers employ the high-level, four-step process below in order to have confidence in the carbon credits that they select.

Undoubtedly, any successful credit purchasing system is dependent on a knowledgeable set of stakeholders. Notably, an entity must align internally on “why" it is interested in purchasing credits and what a credit purchase or credit target will mean for its broader sustainability strategy.

As a company proceeds to reduce its emissions, carbon credits can be used to compensate for the emissions it has yet to cut and/or carbon dioxide removals (CDRs) can be used to address un-abatable emissions, as recommended by the Science Based Targets Initiative (SBTi). The SBTi states that companies should seek to achieve “beyond value chain mitigation" (BVCM), which is inclusive of purchasing carbon credits (such as credits from forest protection (REDD+) or CDRs from direct air capture projects), to finance climate action outside of their value chain. The SBTi Net Zero guidance recommends BVCM as the second step in the mitigation hierarchy after emission reductions, and emphasises that this is a critical component in our societal ambitions for addressing climate change.

Aligning with the SBTi Net Zero guidance is an example of a carbon compensation goal that a corporation may set; however, entities can possess a variety of valid motivations outside of these for purchasing credits, whether that be a bespoke target or an ambition nested into a broader sustainability strategy.

Furthermore, carbon compensation targets may be achieved in different ways depending on a company's motivations. Businesses may wish to align their credit purchases with their social impact ambitions (e.g. a company that produces women's products may be interested in projects with credits that have co-benefits that align with Sustainable Development Goal 5 - Gender Equality & Women's Empowerment) or their value chain (e.g. a company that sells paper products may be interested in forestry credits).

Outside of distilling their key motivations, stakeholders should be educated about the differences between credit types (e.g., nature-based, technology-based), about the market, and about purchasing considerations. Being well-versed in these topics is essential for strong decision-making and ensuring that ambitions are realised.

When an entity formally takes stock of its motives for credit purchases and pairs this with robust credit education, it should then combine these into a formally identified purchasing objective. A strong credit objective will include any budgetary guidelines, the required purchasing volume, and any desired branding alignment (e.g. credits associated with the entity's value chain and considerations for social impact ambitions).

There are a variety of factors to take into account when purchasing credits, which range from alignment with certain standards, to desired co-benefits, geographical preferences, and the quality of the project management, among others.

However, the prioritisation and risk tolerance for each of these considerations will vary from stakeholder to stakeholder and entity to entity. As such, internal stakeholders should seek to develop a consensus on such factors. From there, an entity can set expectations regarding their risk threshold for key considerations.

For instance, consider an entity that is intending to purchase credits, and is deciding how to prioritise various criteria. Within its review, it may realise that nature based solutions (NBS) often have more permanence risk than other credit types, while different geographies may pose a variety of risks based on the governance and legal structures inherent to a country or region. Meanwhile, a less-well established or controversial standard, or even the credit type itself may pose reputational concerns (e.g., credits that have been rejected by certain regulatory or industry standards may be seen as less favourable by others in the broader carbon market). An entity exposed to such considerations must understand both the underlying drivers of such risk and use that understanding to quantify its tolerance for them.

Following our example, the buyer may choose to be open to some governance risk, but only in select geographies. They may be willing to tolerate some permanence risk in nature based projects, but not in any geographies prone to climate-related disasters (e.g. wildfires). Perhaps they will select a certain standard or set of project partners to further screen out credits and align with their preferred risk tolerance. Sophisticated buyers may choose to parse out more nuanced criteria that speak to the intersections with this risk. In this instance, the buyer may be open to purchasing an NBS credit in an area with permanence concerns (e.g. high wildfire risk) if that credit is located in a geography with exceptional government systems and is developed with high-reputation project partners under a preferred standard. The idea here is that the low risk of certain factors (or, specifically, factors that are more important to the entity) balance out the overall risk profile of the purchase, even if the purchase does also embody some riskier characteristics.

There are a number of benefits to this exercise. Firstly, it allows for a clear alignment of key priorities and their justification. More importantly, it allows for an entity to be more nimble in a quickly changing and complex market. With credits frequently becoming unavailable through the duration of a long RFP process, entities are able, by clearly delineating their priorities with a set of purchasing criteria, to efficiently sort through a market that may not have exactly what they want.

Based on the established criteria, entities should consolidate their findings into a clear ask for the credit retailers.

While entities may need months to get internal alignment on selecting carbon credits, typically the carbon market does not allow for credit retailers to hold offered credits firmly for months on end. For this reason, it is necessary for purchasers to build a selection process to account for the fact that most credit retailers won't provide firm offers for more than 10-20 business days. It's understandable that stakeholders may have a number of questions when it comes to the carbon projects offered. However, they shouldn't expect the carbon retailer to answer all of those questions during the duration of the firm offer. It's important for buyers to parse out the questions that need to go to the carbon retailer during the time the credits are on offer versus the questions buyers need answers on prior to going to market. This will help to streamline the purchasing process and build internal carbon education.

Entities should focus credit retailer questions on project-specific concerns, such as:

In order to move swiftly in a market where credits are often quickly snapped up, South Pole recommends avoiding long RFP processes, and instead establishing T&Cs in advance and structuring the ask in such a way that a yes/no decision may be easily determined so as to secure credits in a competitive market. Depending on how an entity approaches its carbon credit purchases, it may consider asking the retailer itself whether its ask is reasonable based on the current market conditions. In the end, it is more efficient for both the retailer and purchaser to course-correct early on and help the purchaser further understand the market.

To ensure the ongoing achievement of climate goals, entities should establish an ongoing system for informed purchasing. By empowering individuals within the entity to continue to operationalize this type of purchasing, an entity can successfully execute credit purchases year after year.

As part of this systemization, entities may consider continuous review, updates, and the establishment of purchasing criteria; formally assigning credit purchasing responsibility to key individuals who continually engage with the market; and ongoing education for purchasers and broader stakeholders in the organisation. Most importantly, entities should be open to giving and receiving feedback. Credit retailers can't improve their offer if they don't know what they could have done better. Likewise, buyers can't improve their credit purchase process if they don't know what's missing the mark.

While the aforementioned process covers the overarching steps required for successful credit review and purchasing, the details of implementation can be complex. South Pole offers advisory services** to help entities build out and implement these purchasing strategies in a way that aligns the credit purchase with their climate goals. Done well, an informed and clear credit purchase system will enable efficient and effective purchase execution. Moreover, it will allow entities to secure the right credits at the right price while also mitigating risk.

*Additionality refers to emissions reductions that would not have occurred without revenue from the sale of carbon credits, permanence refers to the durability of the carbon credit, and leakage refers to the shifting of emissions from the location of the carbon credit project to an unprotected place

**South Pole's credit advisory services do not include soliciting RFPs on behalf of end buyers